스타트업얼라이언스(센터장 이기대)는 지난 19일 ‘2024 한국의 CVC들: 현황과 투자 활성화 방안’이라는 제목의 리포트를 발간했다고 밝혔다.

이번 리포트는 국내 기업형 벤처캐피탈(CVC, Corporate Venture Capital)의 투자 현황과 변화 양상을 심층적으로 분석하고, 향후 정책적·제도적 보완 방향을 제시하고자 기획됐다. 연구책임자는 강신형 충남대학교 경영학부 교수가 맡았고, 분석에는 더브이씨(The VC)의 한국 스타트업 데이터베이스를 활용했다.

CVC는 기업이 스타트업에 투자하는 모험자본(Venture Capital)과 이를 운용하는 조직 전반을 의미한다. 그러나 국내에서는 CVC를 ‘기업이 출자해 설립한 별도의 투자회사’로 좁게 정의하는 경향이 있다. 이에 스타트업얼라이언스는 이번 보고서에서 ▲독립법인 CVC(비금융 일반기업이 출자하여 별도로 설립한 독립적인 투자회사와 이 투자회사가 운용하는 자금) ▲사내부서 CVC(비금융 일반기업이 스타트업에 투자하는 사내 자금과 이 자금을 집행하는 부서) ▲펀드출자 CVC(비금융 일반기업이 기존 민간VC가 결성하는 펀드의 LP출자금)로 유형을 구분하고, 독립법인 CVC와 사내부서 CVC를 중심으로 국내 CVC 생태계를 포괄적으로 분석했다.

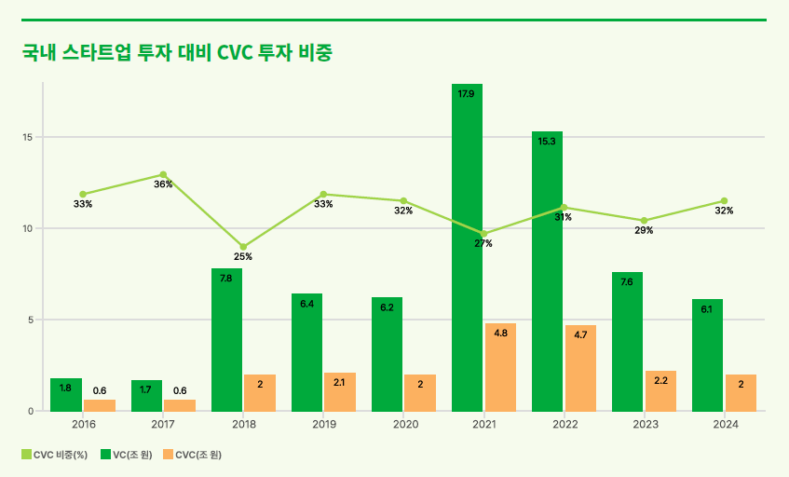

국내 CVC 투자 비중은 결코 낮지 않다. 리포트에 따르면 2024년 국내 CVC 투자금액은 전체 스타트업 투자의 32%를 차지해, 글로벌 평균(26%)과 미국(29%)보다 높은 수준을 기록했다. 하지만 글로벌과 미국 시장에서 CVC 투자가 점차 회복세를 보이는 것과 달리, 국내에서는 여전히 투자 위축이 이어지는 모습이다. 실제로 2024년 3분기까지 글로벌 CVC 투자규모는 전년 대비 10%, 미국은 24% 증가한 반면, 국내는 9% 감소했다.

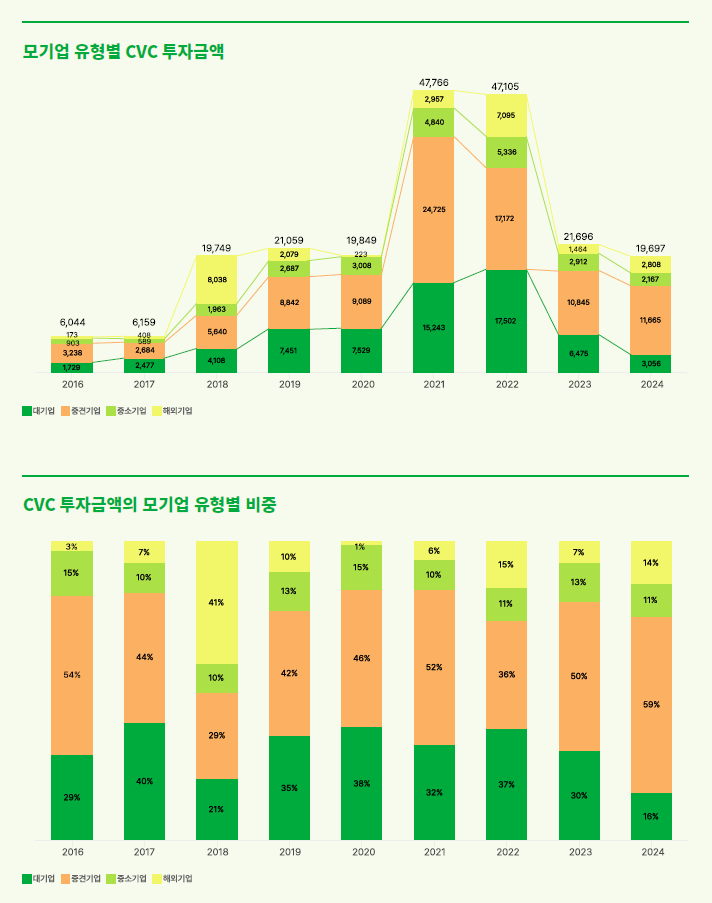

특히 대기업 중심의 CVC 투자 감소가 두드러진다. 2022년과 비교해 2024년 대기업 CVC 투자금액은 1/5 수준으로 축소됐고, 사내부서형 CVC의 경우 무려 1/10 수준까지 급감했다. 경기 침체 영향도 있지만, 대기업들이 전략적 투자 성과에 한계를 느끼며 투자를 조정한 결과로 풀이된다.

반면 중견기업 CVC 투자는 증가했다. 2024년 중견기업의 CVC 투자 비중은 59%까지 확대됐으며, 크래프톤·엔씨소프트 등 주요 중견기업들이 적극적인 투자에 나선 것이 주요 요인으로 분석된다. 다만 다수의 중견기업들은 여전히 스타트업 정보 부족과 협업 파트너 발굴의 어려움을 호소하고 있어, 이에 대한 정책적 지원이 필요하다는 지적도 담겼다.

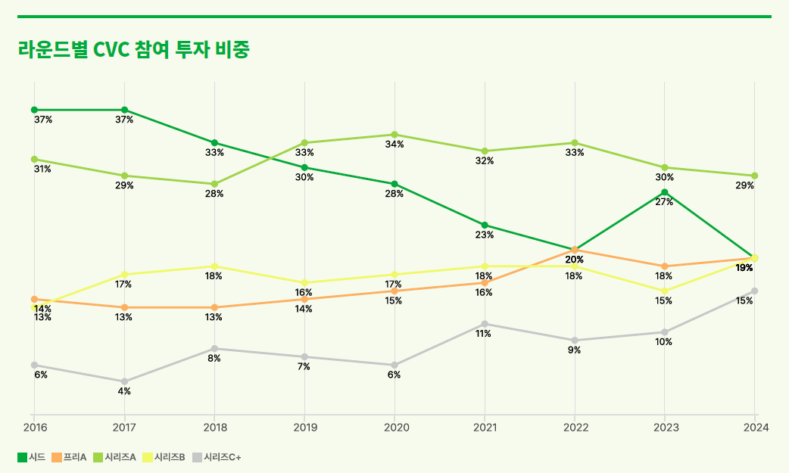

CVC의 투자 행태 변화도 뚜렷하게 나타났다. 과거 기술 선점과 옵션 확보 성격이 강했던 초기(시드) 투자 비중은 감소하는 반면, 후기(시리즈 B·C 이상) 투자 비중은 증가하는 경향이 확인됐다. 이는 단순한 기술 확보를 넘어, 실질적인 사업적 시너지를 창출할 수 있는 성장 단계의 스타트업으로 투자 전략이 변화하고 있음을 보여준다.

산업별 현황에서는 바이오·의료·헬스케어 분야가 2018년부터 2024년까지 가장 많은 투자가 이루어진 것으로 나타났고, 뒤를 이어 게임, 모빌리티, 금융, 콘텐츠 순이었다. 특히 금융 분야는 최근 투자 감소가 두드러져 2024년에는 Top 10 투자 분야에서 제외되었다. 반면, 엔터프라이즈·보안, 음식·외식 분야는 꾸준히 Top 10에 포함되며 안정적인 투자가 지속되고 있는 것으로 나타났다.

리포트는 국내 CVC 생태계의 지속적인 성장을 위해 정책 개선이 필요하다고 강조했다. 구체적으로는 ▲사내부서 CVC에 대한 정책적 관심 및 지원 제고, ▲독립법인 CVC의 오픈이노베이션 연계 유도, ▲중견기업의 오픈이노베이션 활성화, ▲투자 행위 제한이 아닌 관리 감독 및 공시 기능 강화 등을 들었다. 특히, 현재 공정거래법상 일반지주 CVC의 행위 제한 규제 대상은 대부분 중견기업이라며 CVC 투자 활성화를 위해서는 정부가 투자 행위를 세부적으로 제한하기보다 관리 감독과 공시 기능을 강화하는 것이 필요하다고 지적했다.

이기대 스타트업얼라이언스 센터장은 “글로벌 고금리가 닥치자 많은 대기업의 사내 투자 조직이 작동을 멈췄다. 전략적 투자자인 CVC 관련 정책도 결국 실수요자인 중견기업 중심으로 가야 함을 시사한다”고 말했다.

스타트업얼라이언스 리포트는 국내 스타트업 생태계와 정책 이슈를 심층 분석하고 대안을 제시하는 보고서로, 전문은 스타트업얼라이언스 홈페이지에서 무료로 열람 및 다운로드할 수 있다.

- 관련 기사 더 보기

“Changes in startup investment strategy, focusing on domestic CVC mid-sized companies and late-stage investments”

Startup Alliance (Director Lee Ki-dae) announced on the 19th that it published a report titled ‘2024 Korea’s CVCs: Current Status and Investment Activation Measures.’

This report was planned to deeply analyze the investment status and changes in domestic corporate venture capital (CVC) and to suggest future policy and institutional supplementary directions. The research director was Professor Kang Shin-hyung of the Department of Business Administration at Chungnam National University, and the analysis utilized The VC’s Korean startup database.

CVC refers to venture capital that companies invest in startups and the overall organization that operates it. However, in Korea, there is a tendency to narrowly define CVC as a 'separate investment company established with investment from a company'. Accordingly, Startup Alliance categorized the types in this report into ▲independent corporate CVC (independent investment company established separately with investment from a non-financial general company and the funds managed by this investment company), ▲internal department CVC (internal funds invested by a non-financial general company in startups and the department that executes these funds), and ▲fund investment CVC (LP investment in a fund formed by an existing private VC by a non-financial general company), and comprehensively analyzed the domestic CVC ecosystem focusing on independent corporate CVC and internal department CVC.

The proportion of domestic CVC investment is by no means low. According to the report, the amount of domestic CVC investment in 2024 will account for 32% of total startup investment, which is higher than the global average (26%) and the US (29%). However, unlike the gradual recovery of CVC investment in the global and US markets, investment in Korea is still shrinking. In fact, by the third quarter of 2024, the global CVC investment volume increased by 10% year-on-year and the US increased by 24%, while the domestic investment decreased by 9%.

In particular, the decline in CVC investment centered on large corporations is notable. Compared to 2022, the amount of CVC investment in large corporations in 2024 has decreased to 1/5, and in-house department-type CVCs have plummeted to 1/10. This is interpreted as a result of large corporations adjusting their investments as they feel the limits of their strategic investment performance, although this is also due to the impact of the economic downturn.

On the other hand, CVC investment in mid-sized companies has increased. The proportion of CVC investment in mid-sized companies has expanded to 59% in 2024, and it is analyzed that the main factor is the active investment by major mid-sized companies such as Krafton and NCSoft. However, many mid-sized companies still complain about the lack of startup information and the difficulty of finding collaboration partners, and it was pointed out that policy support is needed for this.

Changes in CVC’s investment behavior were also evident. The proportion of early (seed) investments, which were previously focused on securing technology and options, decreased, while the proportion of later (series B, C, and above) investments increased. This shows that investment strategies are changing beyond simple technology acquisition to startups in the growth stage that can create real business synergies.

In terms of industry status, the bio/medical/healthcare sector was shown to have the most investment from 2018 to 2024, followed by games, mobility, finance, and content. In particular, the finance sector has recently shown a notable decrease in investment, and was excluded from the top 10 investment sectors in 2024. On the other hand, the enterprise/security and food/restaurant sectors have consistently been included in the top 10, showing continued stable investment.

The report emphasized that policy improvement is necessary for the sustainable growth of the domestic CVC ecosystem. Specifically, ▲increased policy interest and support for CVCs in internal departments, ▲inducing open innovation linkages of independent corporate CVCs, ▲activating open innovation in mid-sized companies, ▲strengthening management supervision and disclosure functions rather than restricting investment activities, etc. In particular, it pointed out that most of the current restrictions on the activities of general holding company CVCs under the Monopoly Regulation and Fair Trade Act are mid-sized companies, and that in order to activate CVC investment, the government needs to strengthen management supervision and disclosure functions rather than restricting investment activities in detail.

Lee Ki-dae, head of the Startup Alliance Center, said, “As global high interest rates hit, many large companies’ in-house investment organizations stopped functioning. This suggests that policies related to CVCs, which are strategic investors, should ultimately focus on mid-sized companies that are actual users.”

The Startup Alliance Report is a report that deeply analyzes the domestic startup ecosystem and policy issues and presents alternatives. The full report can be viewed and downloaded for free on the Startup Alliance website.

- See more related articles

「スタートアップ投資戦略変化、国内CVC中堅企業・後期投資集中」

スタートアップアライアンス(センター長イ・ギデ)は去る19日'2024韓国のCVCら: 現況と投資活性化案'というタイトルのレポートを発刊したと明らかにした。

今回のレポートは、国内企業型ベンチャーキャピタル(CVC、Corporate Venture Capital)の投資現況と変化の様相を深く分析し、今後の政策的・制度的補完方向を提示しようと企画された。研究責任者は江新型忠南大学経営学部教授が務め、分析にはダブイ氏(The VC)の韓国スタートアップデータベースを活用した。

CVCは、企業がスタートアップに投資する冒険資本(Venture Capital)とそれを運用する組織全体を意味する。しかし、国内ではCVCを「企業が出資して設立した別途投資会社」と狭く定義する傾向がある。スタートアップアライアンスは今回の報告書で▲独立法人CVC(非金融一般企業が出資して別途設立した独立投資会社とこの投資会社が運用する資金) LP出資金)でタイプを区分し、独立法人CVCと社内部署CVCを中心に国内CVCエコシステムを包括的に分析した。

国内CVC投資の割合は決して低くない。レポートによると、2024年の国内CVC投資金額は全体のスタートアップ投資の32%を占め、グローバル平均(26%)と米国(29%)より高い水準を記録した。しかし、グローバルと米国市場でCVC投資が徐々に回復傾向を見せるのとは異なり、国内では依然として投資萎縮が続く姿だ。実際、2024年第3四半期まで、グローバルCVC投資規模は前年比10%、米国は24%増加したのに対し、国内は9%減少した。

特に大企業中心のCVC投資の減少が目立つ。 2022年と比較して2024年大企業CVC投資金額は1/5水準に縮小され、社内部署型CVCの場合、なんと1/10水準まで急減した。景気後退の影響もあるが、大企業が戦略的投資成果に限界を感じて投資を調整した結果として解釈される。

一方、中堅企業のCVC投資は増加した。 2024年中堅企業のCVC投資比重は59%まで拡大され、クラフトン・エンシーソフトなど主要中堅企業が積極的な投資に乗り出したことが主要要因と分析される。ただし、多数の中堅企業は依然としてスタートアップ情報不足と協業パートナー発掘の困難を訴えており、これに対する政策的支援が必要だという指摘も盛り込んだ。

CVCの投資行動の変化も明らかに現れた。過去の技術先占とオプション確保の性格が強かった初期(シード)投資の割合は減少する一方、後期(シリーズB・C以上)の投資の割合は増加する傾向が確認された。これは、単純な技術確保を超えて、実質的な事業的相乗効果を創出できる成長段階のスタートアップで投資戦略が変化していることを示している。

産業別の現況では、バイオ・医療・ヘルスケア分野が2018年から2024年までに最も多くの投資が行われたことが分かり、後に続いてゲーム、モビリティ、金融、コンテンツの順だった。特に金融分野は最近投資減少が目立っており、2024年にはTop 10投資分野から除外された。一方、エンタープライズ・セキュリティ、食品・外食分野は着実にトップ10に含まれ、安定的な投資が続いていることが分かった。

報告書は、国内CVCエコシステムの継続的な成長には政策改善が必要であると強調した。具体的には▲社内部門CVCに対する政策的関心及び支援の向上、▲独立法人CVCのオープンイノベーション連携誘導、▲中堅企業のオープンイノベーション活性化、▲投資行為制限ではなく管理監督及び公示機能強化などを挙げた。特に、現在の公正取引法上、一般持株CVCの行為制限規制対象はほとんど中堅企業であり、CVC投資活性化のためには政府が投資行為を詳細に制限するよりも管理監督と開示機能を強化することが必要だと指摘した。

イ・ギデスタートアップアライアンスセンター長は「グローバル高金利が迫ると多くの大企業の社内投資組織が作動を止めた。戦略的投資家であるCVC関連政策も結局ミス要者である中堅企業中心に行かなければならないことを示唆する」と話した。

スタートアップアライアンスレポートは、国内のスタートアップエコシステムと政策課題を深く分析し、代替案を提示するレポートで、専門はスタートアップアライアンスホームページから無料で閲覧およびダウンロードすることができる。

- 関連記事をもっと見る

“初创企业投资策略转变,重点关注国内CVC中型企业和后期投资”

创业联盟(理事长李基大) 19日发布了一份题为《2024韩国CVC:现状与投资激活措施》的报告。

本报告旨在深入分析国内企业风险投资(CVC)的投资现状及变化情况,并提出未来政策及制度补充方向。该项研究由忠南大学经营系教授姜信亨 (Kang Shin-hyung) 主导,分析利用了 The VC 的韩国初创企业数据库。

CVC是风险投资,即企业对创业公司进行的投资,以及对其进行管理的整体组织。然而,在韩国,有将CVC狭义地定义为‘企业出资设立的独立投资公司’的倾向。因此,Startup Alliance在本报告中将CVC的种类分为▲独立企业CVC(由非金融一般企业出资设立的独立投资公司及其管理的基金)、▲部门内CVC(非金融一般企业向创业公司及其执行部门投资的内部基金)、▲基金投资型CVC(非金融一般企业向已有民间VC设立的基金进行LP出资),并以独立企业CVC和部门内CVC为中心,对韩国CVC生态圈进行了综合分析。

国内CVC投资占比并不低。报告显示,2024年国内CVC投资将占初创企业总投资的32%,高于全球平均水平(26%)和美国(29%)。不过,在全球及美国市场CVC投资逐渐复苏的同时,国内投资仍在萎缩。事实上,截至2024年第三季度,全球CVC投资额同比增长10%,其中美国增长24%,而国内投资则减少9%。

尤其以大企业为中心的CVC投资下滑较为明显。与2022年相比,2024年大型企业的CVC投资金额已降至1/5,企业内部CVC投资则暴跌至1/10。虽然经济衰退确实产生了影响,但这被解读为大公司在感受到其战略投资绩效的极限后调整投资的结果。

另一方面,CVC对中型公司的投资有所增加。 2024年CVC对中型公司的投资占比预计将增至59%,分析认为Krafton、NCSoft等主要中型公司的积极投资是主要因素。但不少中小企业仍抱怨创业信息匮乏、寻找合作伙伴困难,并指出这方面需要政策支持。

CVC投资行为的变化也很明显。早期(种子)投资的比例一直在下降,而早期投资主要集中在获得技术和期权,而后期(B 轮、C 轮或更高轮)投资的比例一直在增加。这表明投资策略正在从简单的技术收购转向能够创造真正业务协同效应的成长期初创企业。

从行业状况来看,2018 年至 2024 年,生物、医疗和保健领域的投资最多,其次是游戏、移动、金融和内容。其中,金融领域近期投资明显下滑,将于2024年被排除在十大投资领域之外。另一方面,企业/安防、食品/餐饮领域则一直稳居前十,投资持续稳定。

报告强调,必须完善政策,确保国内CVC生态系统的持续增长。具体而言,▲加大对部门内CVC的政策关注与支持、▲鼓励与独立企业CVC进行开放式创新联动、▲激活中型企业的开放式创新、▲强化管理、监督和公开职能而非限制投资活动等。他特别指出,现行公平交易法对一般控股公司CVC活动的限制对象大多为中型企业,政府为激活CVC投资,需要强化管理、监督和公开职能而非具体限制投资活动。

创业企业联盟中心主任李基大表示:“随着全球高利率的冲击,许多大公司内部的投资机构停止运作。这表明,作为战略投资者的CVC相关政策最终应该将重点放在作为实际用户的中型企业上。”

《创业联盟报告》是一份深入分析国内创业生态系统和政策问题并提出替代方案的报告。完整报告可在创业联盟网站上免费查看和下载。

- 查看更多相关文章

« Changements dans la stratégie d'investissement des startups, en se concentrant sur les entreprises nationales de taille moyenne et les investissements en phase de développement »

Startup Alliance (directeur Lee Ki-dae) a annoncé le 19 la publication d'un rapport intitulé « CVC coréens 2024 : état actuel et mesures d'activation des investissements ».

Ce rapport a été conçu pour analyser en profondeur l’état des investissements et les aspects changeants du capital-risque des entreprises nationales (CVC) et pour suggérer des orientations politiques et institutionnelles complémentaires futures. La recherche a été menée par le professeur Kang Shin-hyung du département d'administration des affaires de l'université nationale de Chungnam, et l'analyse a utilisé la base de données des startups coréennes de The VC.

CVC fait référence au capital-risque, qui est l'investissement réalisé par les entreprises dans les startups et l'organisation globale qui le gère. Français Cependant, en Corée, il existe une tendance à définir étroitement le CVC comme une « société d'investissement distincte établie avec un investissement d'entreprise ». En conséquence, Startup Alliance a classé les types de CVC dans ce rapport en ▲CVC d'entreprise indépendants (sociétés d'investissement indépendantes établies séparément avec un investissement de sociétés générales non financières et les fonds gérés par ces sociétés d'investissement), ▲CVC de département interne (fonds internes investis par des sociétés générales non financières dans des startups et les départements qui exécutent ces fonds), et ▲CVC de contribution de fonds (contributions LP par des sociétés générales non financières à des fonds formés par des VC privés existants), et a analysé de manière exhaustive l'écosystème national des CVC en se concentrant sur les CVC d'entreprise indépendants et les CVC de département interne.

La part des investissements nationaux dans les CVC n’est en aucun cas faible. Selon le rapport, en 2024, les investissements nationaux en CVC représenteront 32 % du total des investissements dans les startups, ce qui est supérieur à la moyenne mondiale (26 %) et aux États-Unis (29 %). Cependant, alors que les investissements CVC se redressent progressivement sur les marchés mondiaux et américains, les investissements nationaux continuent de diminuer. En fait, au troisième trimestre 2024, le volume mondial des investissements en CVC a augmenté de 10 % en glissement annuel, de 24 % aux États-Unis, tandis que les investissements nationaux ont diminué de 9 %.

En particulier, le déclin des investissements en CVC centrés sur les grandes entreprises est notable. Par rapport à 2022, le montant des investissements CVC dans les grandes entreprises en 2024 a diminué à 1/5, et les investissements CVC internes ont chuté à 1/10. Bien que le ralentissement économique ait eu un impact, il est interprété comme le résultat d’un ajustement des investissements par les grandes entreprises, qui ressentent les limites de la performance de leurs investissements stratégiques.

En revanche, les investissements de CVC dans les entreprises de taille moyenne ont augmenté. La proportion d'investissements CVC dans les entreprises de taille moyenne en 2024 devrait augmenter à 59 %, et l'investissement actif des grandes entreprises de taille moyenne telles que Krafton et NCSoft est analysé comme étant le principal facteur. Cependant, de nombreuses entreprises de taille moyenne se plaignent encore d’un manque d’informations sur les startups et de difficultés à trouver des partenaires de collaboration, et il a été souligné qu’un soutien politique est nécessaire à cet égard.

Les changements dans le comportement d’investissement de CVC étaient également évidents. La proportion d’investissements précoces (d’amorçage), qui étaient auparavant axés sur la sécurisation de la technologie et des options, a diminué, tandis que la proportion d’investissements ultérieurs (séries B, C ou supérieures) a augmenté. Cela montre que la stratégie d’investissement évolue au-delà de la simple acquisition de technologies vers des startups en phase de croissance qui peuvent créer de réelles synergies commerciales.

En termes de statut industriel, les secteurs bio, médical et de la santé ont connu le plus d'investissements de 2018 à 2024, suivis des jeux, de la mobilité, de la finance et du contenu. En particulier, le secteur financier a récemment connu une baisse notable des investissements et sera exclu du top 10 des secteurs d’investissement en 2024. En revanche, les secteurs des entreprises/sécurité et de l’alimentation/restauration ont toujours été inclus dans le top 10, affichant un investissement stable et continu.

Le rapport souligne que des améliorations politiques sont nécessaires pour assurer la croissance continue de l’écosystème national des CVC. Français Plus précisément, ▲ accroître l'intérêt politique et le soutien aux CVC dans les départements internes, ▲ encourager les liens d'innovation ouverte avec les CVC d'entreprise indépendants, ▲ activer l'innovation ouverte dans les entreprises de taille moyenne, ▲ renforcer les fonctions de gestion, de supervision et de divulgation plutôt que de restreindre les activités d'investissement, etc. En particulier, il a souligné que la plupart des sujets des restrictions actuelles de la loi sur le commerce équitable sur les activités des CVC de sociétés holding générales sont des entreprises de taille moyenne, et que pour activer l'investissement dans les CVC, le gouvernement doit renforcer ses fonctions de gestion, de supervision et de divulgation plutôt que de restreindre les activités d'investissement en détail.

Lee Ki-dae, directeur du Startup Alliance Center, a déclaré : « Avec la hausse des taux d'intérêt mondiaux, les organisations d'investissement internes de nombreuses grandes entreprises ont cessé de fonctionner. Cela suggère que les politiques relatives aux CVC, qui sont des investisseurs stratégiques, devraient à terme se concentrer sur les entreprises de taille moyenne qui sont de véritables utilisatrices. »

Le rapport Startup Alliance est un rapport qui analyse en profondeur l’écosystème national des startups et les problèmes politiques et présente des alternatives. Le rapport complet peut être consulté et téléchargé gratuitement sur le site Web de Startup Alliance.

- Voir plus d'articles connexes

You must be logged in to post a comment.